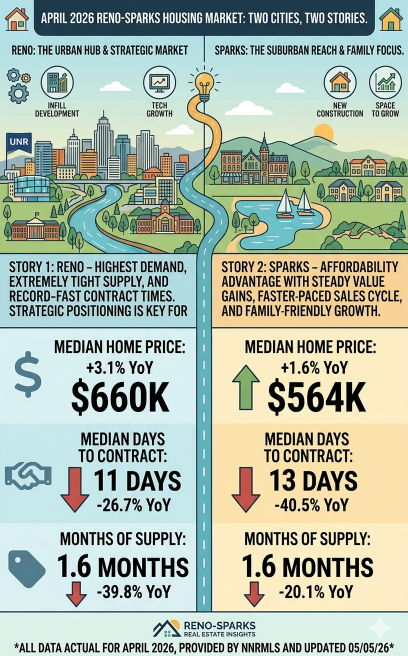

- Reno's median sales price hit $660,000 in April 2026 — up 4.5% from March in a single month and up 3.1% year over year. Closed sales surged 29.4% above April 2025.

- Sparks held its median at $564,000 — flat from March, up 1.6% year over year — but registered the first real inventory uptick of the spring. Months supply rose to 1.6, up 25.5% from March.

- Both cities remain firmly seller-side. Reno sellers received 99.0% of list price; Sparks sellers received 99.4%. Median days to contract: 11 in Reno, 13 in Sparks.

- The Freddie Mac 30-year mortgage rate sat at 6.37% on May 7, 2026 — 39 basis points below where it was a year ago. Buyer purchasing power has quietly improved.

- Anyone reading "market softening" national headlines should look at the Reno number first. A median up 4.5% in a single month, an 11-day pace, and sellers walking away with 99 cents on every list-price dollar is not a softening market.

April's numbers landed last week, and the spring story that started in March turned into something stronger — but not in the way most national headlines would lead you to expect. Reno-Sparks does not function as one market anymore, and April made that impossible to ignore. The two cities posted very different numbers, told very different stories, and put very different choices in front of sellers thinking about listing this spring.

Here is what the Northern Nevada Regional MLS data, updated May 5 via Domus Analytics, actually shows.

Reno: Accelerating

Reno's median sales price reached $660,000 in April 2026 — up 4.5% from March in a single month, and up 3.1% year over year. That 4.5% one-month jump is the largest single-month gain of 2026. It builds directly on the trajectory we covered in our March 2026 market update.

The activity figures tell the rest of the story. Closed sales totaled 299 single-family homes — up 16.8% from March and 29.4% from April 2025. The median home went under contract in 11 days, the fastest pace recorded this year and a 26.7% improvement on both March and year-ago figures.

New listings rose to 398, up 6.4% from March. That sounds like inventory relief. It wasn't. Active inventory ended April at 481 homes — only 0.8% above March, and still down 22.0% from a year ago. Buyers absorbed the new supply almost as fast as it arrived. Sellers received 99.0% of list price, and median sold price per square foot reached $345, up 3.6% from March.

For sellers in Somersett, Damonte Ranch, Caughlin Ranch, ArrowCreek, Southwest Reno, and Northwest Reno, this is the environment your home enters if you list now. A well-prepared, correctly priced home is not arriving into a sea of competition — it is arriving into a market that has been waiting for it.

Sparks: Taking a Breath

Sparks tells a different story, and reading it correctly matters.

The Sparks median sales price closed April at $564,000 — flat from March (down 0.2%), but up 1.6% from a year ago. Closed sales fell to 135, down 12.9% from March and 6.9% from April 2025. At first glance, that looks like softening. It isn't.

Median days to contract held at 13 — still 40.5% faster than a year ago. Sellers received 99.4% of list price, slightly higher than Reno's 99.0%. Active inventory rose to 212 homes (up 9.3% from March), and months supply moved to 1.6 (up 25.5% from March, but down 20.1% year over year).

What that combination describes is normalization, not softening. Sparks was operating so tight earlier this spring that any rebalance produced large percentage moves — and going from 1.3 to 1.6 months of supply is the difference between extreme scarcity and ordinary scarcity, not the difference between a seller's market and a buyer's market. Well-prepared homes in Wingfield Springs, Spanish Springs, and the Sparks Galleria corridor are still pricing in the high 99s and going under contract in under two weeks. A balanced market — by the technical definition — runs four to six months of supply. Sparks closed April at 1.6.

The Rate Environment in May 2026

The Freddie Mac Primary Mortgage Market Survey released May 7, 2026 showed the 30-year fixed-rate mortgage averaging 6.37% — up from 6.30% the prior week, but down from 6.76% a year ago. Sam Khater, Freddie Mac's Chief Economist, noted that "recent data points to slightly better conditions for buyers with a boost in new-home sales, median new-home prices being down to their lowest level since July 2021, and higher inventory than in recent years."

Run the math at the Reno median. A buyer at $660,000 with 20% down carries a loan of roughly $528,000. At today's 6.37% rate, principal and interest runs approximately $3,290 per month. At April 2025's 6.76% rate, the same loan would have run approximately $3,430 per month. That is about $140 less per month — roughly $1,700 per year — for the same buyer entering today's market versus a year ago. (These figures are illustrative; actual payments depend on lender, credit score, down payment, and loan terms.)

The point isn't that rates are low. They aren't. The point is that affordability has quietly improved year over year. The buyer pool active in Reno-Sparks right now has either processed that improvement, or carries enough equity from a prior sale — typically from California, Washington, or Oregon — that rate moves do not materially shape their offer.

What April Actually Means for Sellers

First, if you have been waiting for spring to "really" arrive, April answered the question. The spring window is not a forecast anymore. It is the present tense.

Second, if you have been waiting for national headlines to confirm that selling is the right move, you are likely going to be waiting a long time. The 2026 national headline cycle has been built on softening Sun Belt markets, Treasury yield volatility, and tariff uncertainty. None of those stories describe what is happening here. Our piece on the Noise Penalty made the case that waiting for national clarity has its own cost — and the April acceleration in Reno is what that cost looks like for a seller who hesitated.

Third — and this is the question we are fielding most often from sellers right now — some version of "are we at peak?"

Nobody knows where peak is in real time. What we do know: Reno's median is accelerating, closed sales are running 29.4% above last year, 1.6 months of supply in both cities is not a market that produces near-term price corrections, and the buyer pool is dominated by well-capitalized buyers whose decisions are not particularly sensitive to small rate moves. The case for selling now is built on data verifiable today. The case for waiting depends on national forecasts that have been wrong three years running.

For homeowners considering whether the market actually rewards a sale right now, the place to start is not an online estimate that flattens neighborhood, condition, and finish into a single algorithmic number. The place to start is a real comparative market analysis.

If you are weighing whether to list your Reno-Sparks home this spring, Robin and Kevin build real comparative market analyses — not algorithm estimates. Request yours at kinneyandrenwickteam.com/home-valuation/, or contact Kevin Kinney at 775-391-8402 or Robin Renwick at 775-813-1255.

Frequently Asked Questions

What is the current median home price in Reno-Sparks in 2026?

As of April 2026, the median single-family home sale price in Reno is $660,000 — up 4.5% from March and 3.1% year over year. In Sparks, the April median was $564,000, flat from March and up 1.6% year over year. Source: NNRMLS via Domus Analytics, updated May 5, 2026.

Is it still a seller's market in Reno-Sparks in May 2026?

Yes — decisively. Both cities closed April at 1.6 months of housing supply, less than half the four-to-six-month range that defines a balanced market. Sellers received 99.0% of list price in Reno and 99.4% in Sparks, with median days to contract at 11 and 13 respectively.

How long does it take to sell a home in Reno-Sparks right now?

In April 2026, the median single-family home went under contract in 11 days in Reno and 13 days in Sparks — the fastest pace recorded this year. Reno's days-to-contract dropped 26.7% from March; Sparks' figure is 40.5% faster than April 2025.

How are mortgage rates affecting Reno-Sparks buyers in May 2026?

The Freddie Mac 30-year fixed-rate mortgage averaged 6.37% as of May 7, 2026 — down from 6.76% a year ago. For a buyer at the Reno median of $660,000 with 20% down, that year-over-year rate improvement reduces principal and interest by approximately $140 per month, or roughly $1,700 annually. Figures are illustrative; actual rates depend on lender, credit, and loan terms.

Why is Sparks showing different numbers than Reno in April 2026?

Sparks recorded the first measurable inventory uptick of the 2026 spring — active inventory up 9.3% from March, months supply up 25.5% to 1.6 months. But pricing held, days to contract stayed at 13, and sellers still received 99.4% of list. This is normalization from extreme tightness, not softening. Sparks remains firmly seller-side.

Is Reno-Sparks part of the national "housing market softening" story?

No. The markets driving national softening narratives are concentrated in Sun Belt metros with multi-month inventory bloat, weakening employment, and over-leveraged new construction pipelines. Reno-Sparks has none of those preconditions. EDAWN's 2026 State of the Economy presentation ranked Reno as the #1 metro for economic growth out of 949 nationally.

Should I sell my Reno-Sparks home in May 2026, or wait?

The April data supports listing now if a sale is the right strategic move for your situation. Reno's median is accelerating. Both cities are at 1.6 months of supply. Sellers are receiving high-99-percent of list. Waiting for "more clarity" has historically cost sellers more than it has saved them, and the national forecasts the wait-it-out narrative relies on have been wrong for three consecutive years.

What is the difference between an online home value estimate and a real CMA?

Online estimates — including the one on our own valuation page — are algorithmic. They aggregate public records and recent sales to produce a number that does not account for your specific finishes, condition, micromarket factors, or current buyer demand. A real comparative market analysis from Robin or Kevin starts from there and adjusts against floor plan, condition, upgrades, lot characteristics, and current active and pending competition.

This article is for general informational purposes only and is not legal, tax, or financial advice. Market conditions change, and the information here may not reflect the most current market data by the time you read it. Automated home value estimates, including the one on our own site, are algorithmic estimates and do not reflect the actual market value of any specific home. For a true comparative market analysis, or for guidance specific to your Reno-Sparks home and situation, contact Kevin Kinney or Robin Renwick directly.

Check out this article next