Disclaimer: This blog is for informational purposes only and does not constitute financial, legal, or investment advice. Market data sourced from Domus Analytics/NNRMLS (March 2026), Freddie Mac Primary Mortgage Market Survey (April 9, 2026), EDAWN 2026 State of the Economy (February 5, 2026), HomeLight Top Agent Insights Survey (fielded December 2025, published April 2, 2026), and Bright MLS Chief Economist commentary (December 2025). Statistics reflect conditions as of publication date and are subject to change. Consult a qualified real estate professional for guidance specific to your property and circumstances.

Key Takeaways

- Freddie Mac's April 9 PMMS shows the 30-year fixed mortgage at 6.37% — down from 6.46% the prior week and 6.62% a year ago — meaning buyer purchasing power is quietly improving even as national headlines scream uncertainty

- National seller hesitation is real and documented, but it's concentrated in markets with inventory bloat, weakening employment, and over-leveraged new construction — not in Reno-Sparks

- The Reno-Sparks market absorbed a 59.8% surge in new spring listings in March without accumulating inventory: 15 days to contract in Reno, 16 in Sparks, with sellers receiving within 1% of asking price

- Reno's ranking as the #1 economic growth metro out of 949 nationally (EDAWN 2026 State of the Economy) insulates local housing demand from purely cyclical national fears — the demand engine here runs on structurally different fuel

- The Noise Penalty is real: every week a well-positioned Reno-Sparks seller waits for national clarity typically means listing into a more competitive spring inventory environment — at reduced negotiating leverage

The week of April 7, 2026 has delivered the full cocktail of economic anxiety in a single sitting. Trade policy is shifting faster than markets can price in — tariff announcements arriving and partially reversing on the same news cycle, Treasury yields spiking to levels not seen in years, and stock indices swinging with a volatility that would have dominated entire months of coverage in any prior decade. Recession odds, depending on which economist you follow and which morning you check, sit somewhere between uncomfortable and alarming. And somewhere in the middle of all of this, a homeowner in Somersett or Caughlin Ranch or Double Diamond is sitting with a listing decision they've been working toward for months, wondering whether now is really the time.

That hesitation is completely understandable. The national economic noise of April 2026 is not manufactured, and taking it seriously is not irrational. The mistake isn't feeling the anxiety. The mistake is assuming that national economic conditions map cleanly onto Reno-Sparks market conditions. They don't. They haven't for years. And the specific forces driving the national fear narrative right now were built around markets that look nothing like what Northern Nevada Regional MLS data has been documenting here for the past six months.

This blog is about that gap — the distance between what the national headlines describe and what the Reno-Sparks data actually shows. It introduces a concept we're calling the Noise Penalty: the specific, measurable cost that accrues when sellers let national economic anxiety govern a local decision that local data consistently does not support.

What's Actually Driving the National Seller Freeze

It's worth naming the fear clearly, because vague anxiety is harder to address than specific claims. The national economic picture in April 2026 combines several forces that don't normally arrive simultaneously, and understanding each one precisely is the first step toward understanding how much of it applies here.

Start with tariffs. The National Association of Home Builders estimated tariff-related material cost increases of approximately $10,900 per new home in direct inputs — lumber, steel, aluminum, gypsum — and subsequent rounds of tariff announcements have pushed those estimates higher. For markets where new construction was doing the heavy lifting on housing supply, that pressure matters enormously. It slows affordable new product entering the market, it creates pricing uncertainty for builders evaluating new starts, and it reduces the competitive advantage that new homes traditionally hold over existing inventory at similar price points. Those effects are real. They are also concentrated in markets that rely on construction pipelines in ways that Reno-Sparks — where active inventory sits at 618 combined listings for a metro of 400,000 — simply does not.

Beyond construction costs, the tariff environment has generated the kind of financial market volatility that bleeds directly into housing psychology. Nearly 70% of homeowners hold equity positions, according to Federal Reserve survey data. When portfolios swing significantly in a single week — as they have in early April — it produces a particular kind of anxiety that isn't specific to housing but influences every major financial decision, including the decision to list. HomeLight's Top Agent Insights Survey, published April 2, 2026 and compiled from more than 850 real estate agents nationally, found that sellers across the country have entered a freeze response. "[With] so much uncertainty in the economy, a lot of people are frozen and afraid to make a move," observed Walt Reinhardt, an Austin, Texas agent quoted in the report. That's not one agent's anecdote. It reflects a pattern playing out nationally in real time.

Then there is the recession conversation itself. Depending on the model and the inputs, recession probability estimates for 2026 range from the low 20s to over 60 percent. That spread reflects genuine uncertainty in the forecasting, not a divide between alarmists and optimists. The factors that would trigger a recession — sustained tariff-induced inflation, corporate margin compression from rising input costs, a consumer pullback driven by wealth effect erosion, and Federal Reserve policy miscalculation — are all present to some degree. They interact with each other in ways that make outcomes genuinely hard to forecast, and that uncertainty is legitimate macroeconomic risk.

Lisa Sturtevant, Chief Economist at Bright MLS, offered the most analytically useful framing for all of this in her 2026 outlook: "Market performance will hinge on local economic conditions, making 2026 one of the most geographically divided markets we've seen in years." That's not a caveat at the bottom of a report. It's the primary lens through which every Reno-Sparks seller should be evaluating the noise they're hearing this week.

The Anatomy of Reno-Sparks Insulation

When economists and real estate analysts point to markets experiencing price softness or demand weakness in 2026, they are describing a recognizable pattern: markets with accumulated inventory, with over-leveraged new construction pipelines, with pandemic-era migration patterns that have since reversed, and with employment bases that lack the structural depth to absorb cyclical softness. Cape Coral. North Port-Sarasota. Parts of Phoenix and suburban Denver. Markets where prices ran ahead of fundamentals on speculative demand and are now correcting toward those fundamentals. Those corrections are real, and the concern they generate in national commentary is appropriate for those markets.

Reno-Sparks does not have those preconditions, and that's not a promotional claim. It's a data claim, and it has been validated quarter after quarter by the same organization — NNRMLS through Domus Analytics — that has no interest in flattering the local market.

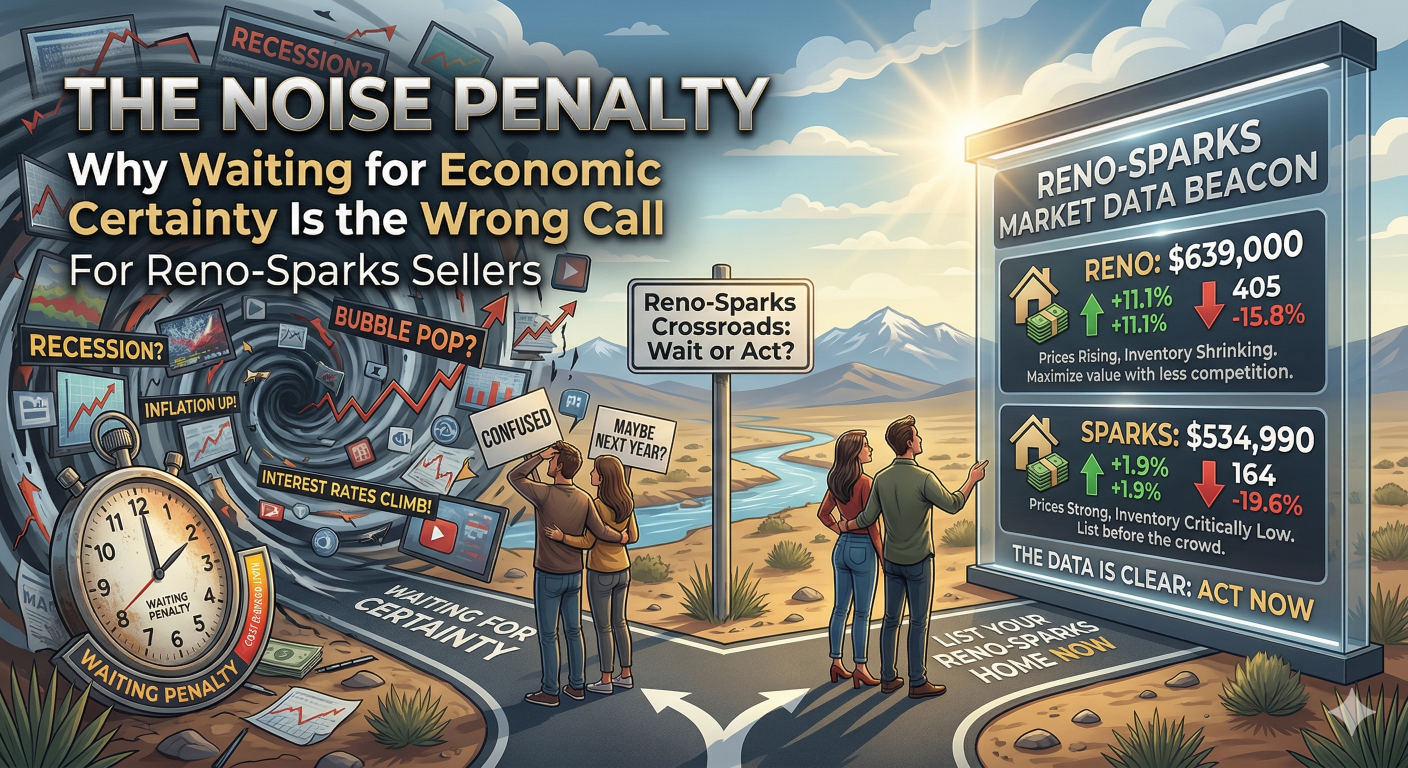

As of March 2026, Reno had 443 active single-family listings. Sparks had 175. Combined: 618 homes available in a metropolitan area of 400,000 people. The threshold that economists use to define a seller's market is six months of supply. Reno is operating at 1.7 months. Sparks is at 1.1 — the tightest reading this market has recorded in the current cycle. We documented the full March picture in our March 2026 market analysis: 255 closings in Reno (up 23.2% from February), 153 in Sparks (up 43.0%), with the Reno median holding at $632,000 and sellers receiving 98.9% of list price. New listings surged 59.8% in Reno from February to March — a volume that in a softening market would have sent active inventory climbing. Instead, active inventory ended March essentially where it began. The market absorbed the listings nearly as fast as sellers could prepare them.

That's the structural fingerprint of a market where demand has been consistently outrunning supply. It is the opposite of what the national softening narrative describes. And it has a specific economic cause that explains why it persists regardless of what national headlines are doing on any given week.

Why Recession Anxiety May Actually Be Helping Reno-Sparks Buyers — And What That Means for Sellers

Here is the counterintuitive dimension of April's economic story that almost never surfaces in the seller conversation, because it requires holding two ideas simultaneously: the same recession anxiety that is generating national fear is also pushing mortgage rates lower, and lower rates expand the pool of qualified buyers for your home.

Freddie Mac's Primary Mortgage Market Survey, released April 9, 2026, showed the 30-year fixed-rate mortgage averaging 6.37% — down from 6.46% the prior week and meaningfully below the 6.62% rate that prevailed a year ago. Sam Khater, Freddie Mac's Chief Economist, noted directly: "Mortgage rates ticked down this week, averaging 6.37%. The decrease in rates represents a positive development for prospective homebuyers and could spark a more favorable spring homebuying season than last year."

The mechanism is worth understanding precisely. When investors become nervous about economic conditions, they historically move capital into the comparative safety of U.S. Treasury bonds. Bond prices rise. Yields fall. And because 30-year mortgage rates track closely with 10-year Treasury yields, rates often decline during periods of elevated recession anxiety — exactly the dynamic playing out right now. The MBA's most recent forecast targets 30-year rates near 6.30% through the remainder of 2026. Fannie Mae projects rates approaching 6% by year-end. Both forecasts assume a continuation of the economic uncertainty that is currently causing seller hesitation.

What does 6.37% mean in actual dollars at Reno-Sparks pricing? On a $632,000 home — Reno's March median — a buyer financing 80% of the purchase price carries a monthly principal and interest payment of approximately $3,125 at 6.37%. At last year's rate of 6.62%, that same payment was approximately $3,192. The difference is $67 per month, or roughly $800 annually — real purchasing power that keeps more buyers financially qualified at Reno-Sparks price points than were qualified six months ago. At the $560,000 Sparks median, the same rate improvement translates to comparable monthly savings on an 80% loan. These aren't dramatic numbers in isolation, but they are the marginal factor that keeps buyers off the fence and active in the market.

The question sellers sometimes ask is whether waiting for rates to drop further might produce a stronger buyer pool in May or June. The honest answer is: possibly, but the conditions that produce lower rates — deepening recession fears, softening employment — also produce the buyer anxiety that offsets much of the purchasing-power benefit. The most favorable seller environment is not the lowest-rate environment in isolation. It's the low-rate environment that precedes broad market awareness of those rates, when buyers are motivated but not yet accompanied by surging competing inventory. That environment exists today. Whether it exists in the same form in six weeks is genuinely uncertain.

The Structural Demand Argument: Why This Market's Buyer Pool Is Different

The reason Reno-Sparks housing demand doesn't dissolve under national economic pressure isn't seasonality or luck. It's economic architecture — a specific set of structural drivers that operate on different fuel than the cyclical, sentiment-based demand that makes national housing statistics volatile.

Kevin attended EDAWN's 2026 State of the Economy presentation on February 5, where Brian Gordon of Applied Analysis and Taylor Adams of EDAWN presented the full regional economic picture. The headline number — Reno as the number-one metro for economic growth out of 949 national metros — doesn't emerge from a single favorable data point. It reflects the convergence of business investment velocity, job creation at above-average wages, venture capital inflows, and technology sector expansion that has been accelerating in Northern Nevada for years. Total business investment in 2025 reached $534 million. New jobs added: 593, at an average salary of $76,800. Organic job creation across the broader economy produced an additional 772 positions. And the venture capital ecosystem — barely a measurable factor in Reno's economy a decade ago — generated $1 billion in total investment over the past year, including $230 million in additional capital and the region's first technology unicorn.

The data center story compounds this in ways that directly affect housing demand's recession resilience. Reno has emerged as the fastest-growing data center hub in the United States, ahead of Salt Lake City, Phoenix, Atlanta, Dallas-Fort Worth, Chicago, Austin, and Denver, with growth of up to 953% in the period tracked by Upwind and JLL's 2024 Data Center Report. Data center construction spending is projected to rise 23% in 2026. This matters for housing because the demand data centers create — for employees, for executives, for the supporting professional class around digital infrastructure — is not discretionary. Cloud computing, artificial intelligence infrastructure, and data processing capacity are not line items companies cut when economic conditions soften. The professionals accepting those positions and the executives relocating their families to manage them need housing in Wingfield Springs, Arrowcreek, and Galena Forest regardless of what the Dow did yesterday.

Migration data reinforces the structural picture. United Van Lines' 2025 National Movers Study placed Nevada tenth nationally for inbound migration. Of those arriving, 20.5% cited family proximity as a primary driver, 19.9% cited retirement, and 19.9% cited job relocation. These aren't people who made spontaneous decisions based on stock market performance. They're executing moves with twelve-to-twenty-four-month planning horizons, and Reno-Sparks is their destination for reasons that predate — and will outlast — the current cycle of tariff headlines.

The buyers currently searching for homes in Spanish Springs, Damonte Ranch, South Reno, and Old Southwest Reno reflect this profile. California equity relocators who have closed Bay Area or Sacramento transactions and are moving $400,000 to $800,000 in housing equity into Reno real estate — for tax structure, lifestyle, proximity to family, and the simple arithmetic of what that equity buys here versus what it buys there. Technology professionals who've accepted positions with data center operators or expanding tech companies, establishing housing before their start dates. Retirees executing a Nevada transition that eliminates state income tax on Social Security, pension distributions, and investment income. Not one of those buyers is checking recession probability models before submitting an offer on a well-prepared home in Northwest Reno. Their motivation exists at a different level than the cycle that generates the national fear narrative.

When the national coverage warns that recession fears are chilling buyer activity, it is describing a specific kind of buyer — first-time purchasers relying on brokerage accounts for down payments, buyers in markets with abundant alternatives, buyers whose purchase is driven primarily by optimism about economic conditions rather than structural life decisions. That buyer exists in every market, including this one. But in Reno-Sparks's upper-mid inventory, that buyer was never the primary demand driver. Their hesitation shows up in the national statistics. It doesn't define the Reno-Sparks reality.

The Noise Penalty: Naming What It Costs to Wait

Every week in April that a well-positioned Reno-Sparks seller spends waiting for economic clarity carries a specific and measurable cost. We're calling it the Noise Penalty.

The mechanism is worth understanding precisely, because it doesn't feel like a cost in real time — it feels like prudence. When national economic anxiety rises, sellers in markets with strong fundamentals tend to pause at roughly the same rate. The hesitation registers internally as responsible financial management: waiting for signals to clear, for conditions to stabilize, for the right moment. What the individual seller doesn't observe in real time is that other sellers in their neighborhood are making identical calculations and breaking from that position at unpredictable intervals. The result is a pattern as reliable as any seasonal trend: spring inventory builds gradually, then surges. When it surges, it changes the competitive landscape for every seller who was waiting.

In March 2026, 366 new listings entered the Reno market in a single month — a 59.8% surge from February. That surge was absorbed almost entirely by existing demand; active inventory barely moved. But March isn't the peak of the spring listing season. April historically produces more new listings than March, and May more than April. The window in which a seller can list against limited competition from comparable homes has an outer edge, and that edge is now visible on the calendar. The sellers entering the market in the next two to three weeks are listing into the best supply-demand conditions of the spring. The sellers who wait another four to six weeks are listing into a market where their neighbors have caught up.

The Noise Penalty shows up in three specific metrics: days on market, list-price ratio, and offer quality. In March 2026, Reno sellers received 98.9% of their list price in a median of 15 days. Those numbers are strong. They reflect the tight supply-demand imbalance that characterizes this market right now. As spring inventory builds, days on market extends incrementally and list-price ratios edge downward — both gradually and then more quickly as the pool of competing listings accumulates. The seller who lists into a 15-day market with seven interested buyers is in a categorically different position than the seller who lists four weeks later into a 30-day market with three. Both are selling the same home. The timing is doing more of the work than either seller realizes.

None of this trajectory is unknowable in advance. It's seasonal, consistent, and well-documented in Reno-Sparks market history. What makes it specifically relevant in April 2026 is that national economic noise is amplifying the hesitation response more than usual — producing more sellers sitting on the sidelines, which means the competitive window for sellers who understand the distinction between national noise and local reality is, if anything, wider than it would be in a quieter news environment. The sellers waiting for the noise to clear are, in effect, preserving the competitive advantage of the sellers who aren't.

The honest version of the Noise Penalty question is this: what is the marginal benefit of waiting one more month for national economic conditions to resolve in a market where those conditions are not the primary driver of outcomes? Based on the data, the marginal benefit is close to zero. The marginal cost — accumulating competing inventory, diminishing urgency in the buyer pool, reduced negotiating leverage — is real and accrues week by week.

A Direct Answer to the Questions Reno-Sparks Sellers Are Actually Asking

There's a specific category of seller this blog was written for — the seller who has already decided, whose life circumstances support a move, whose equity position is strong, and whose home is well-suited to the current buyer profile — and who is pausing because the news is loud. For that seller, the most useful thing we can offer is direct answers rather than another layer of abstraction.

Will recession cause Reno-Sparks home prices to fall significantly? For this to happen, the market would need to experience one of two conditions: a sustained demand collapse that leaves listings sitting unsold, or a surge of distressed inventory from owners who can't maintain their payments. Neither condition exists here. Equity is strong across the Reno-Sparks homeowner base — sellers who purchased between 2015 and 2020 are sitting on six-figure appreciation with low-rate mortgages. The demand that would need to collapse is anchored in structural economic growth that is not cyclical. And at 1.7 months of supply in Reno and 1.1 in Sparks, there is no inventory overhang waiting to express itself as downward price pressure. There is no credible mechanism for a meaningful price correction in this market under current conditions.

Will stock market volatility reduce the quality of offers I receive? Not for the buyer profile that dominates Reno-Sparks upper-mid demand. A California equity buyer arriving with $500,000 or $600,000 from a Bay Area sale isn't funding a down payment from a brokerage account. Their financial position is anchored in home equity — a durable asset that doesn't swing with the Nasdaq. The stock market volatility that creates anxiety for first-time buyers piecing together down payments from investment accounts has a different relationship with the buyers submitting offers on $700,000 homes in Somersett or Caughlin Ranch. For those buyers, the more relevant risk is waiting too long and finding the home they wanted already under contract.

Should I wait for rates to improve further? Rates are 6.37% today, down from 6.62% a year ago. The direction has been favorable. Whether rates will be meaningfully lower in six weeks is genuinely uncertain — the same economic conditions that push rates down also produce the buyer anxiety that offsets part of the purchasing-power benefit. What is certain is that the buyer pool at today's rates is active, qualified, and operating in a supply environment that gives them limited choices. That combination is exactly what produces the list-price ratios and days-to-contract figures that Reno-Sparks sellers have been seeing all spring. Waiting for rates to improve is a bet that the conditions producing today's favorable outcomes will be even more favorable in a month — a bet that local market history doesn't support and that national economic uncertainty makes genuinely unpredictable.

The broader answer is that the case for listing now in Reno-Sparks is not built on optimism or promotional positioning. It's built on specific, verifiable data about supply, demand, pricing velocity, and the structural characteristics of a regional economy that has earned its number-one national growth ranking through investment and job creation that predate the current tariff calendar and will outlast it. Those factors don't become less true because the national headlines are loud. In some respects, they become more relevant — because the louder the national noise, the clearer the gap between what the headlines describe and what the Reno-Sparks data actually shows.

The Noise Penalty doesn't care about intention. It doesn't distinguish between sellers who paused for good reasons and sellers who paused for poor ones. It accumulates the same way for all of them, week by week, in the form of additional competing listings and incrementally reduced leverage. For sellers in neighborhoods like Rancharrah, Midtown, South Meadows, or Galena Forest who have been working toward a spring listing — the local data is not sending a cautious signal. It's sending a clear one.

If you're considering a strategic sale or want a thoughtful conversation about what the current environment means for your specific property and timeline, we're happy to talk through your goals. Contact Kevin Kinney at 775-391-8402 or Robin Renwick at 775-813-1255.

Frequently Asked Questions

1. Will the 2026 recession fears actually cause home prices to fall in Reno-Sparks?

For a meaningful price correction to occur in Reno-Sparks, the market would need either a sustained demand collapse or a surge of distressed inventory — neither of which exists in a market running at 1.7 months of supply (Reno) and 1.1 months (Sparks) with sellers receiving 98-99% of list price. The demand base is anchored in structural economic drivers — data center employment, tech sector relocation, California equity migration — that operate on longer planning horizons than a recession quarter. The Reno metro ranked first for economic growth out of 949 national metros per EDAWN's 2026 analysis. That structural foundation insulates this market from the purely cyclical demand softness that is producing price corrections in over-inventoried Sun Belt markets.

2. Should I wait for mortgage rates to drop before listing my Reno-Sparks home?

Rates are 6.37% as of April 9, 2026 — down from 6.62% a year ago and the lowest reading in the current rate cycle. The conditions most likely to produce further rate declines (recession onset, Fed intervention) are also the conditions that generate buyer anxiety and potentially reduce offer quality. The most favorable seller environment isn't the lowest-rate environment in isolation; it's the low-rate environment paired with tight supply and motivated buyers — which describes Reno-Sparks right now. Waiting for rates to drop further is a bet on future conditions that is uncertain and carries a specific cost: additional competing listings entering the spring market week by week.

3. How is Reno-Sparks different from national housing markets seeing price declines?

The markets experiencing price softness in 2026 share common characteristics: inventory above six months of supply, over-leveraged new construction pipelines, reversed migration patterns, and employment bases without the structural depth to absorb cyclical softness. Reno-Sparks has the opposite conditions — 1.7 months of supply in Reno, 1.1 in Sparks, structural demand anchored in data center employment and California equity relocation, and a regional economy ranked first nationally for growth. The national softening narrative applies to specific markets. Reno-Sparks's data has been consistently pointing in the opposite direction for the past twelve months.

4. What is the "Noise Penalty" for Reno-Sparks sellers?

The Noise Penalty is the measurable cost sellers incur when they allow national economic noise to delay a listing decision that local market data does not support. In Reno-Sparks, spring inventory builds week by week — March saw 366 new Reno listings enter the market in a single month, a 59.8% surge from February. Sellers who list during the early-spring window capture maximum demand with minimum competition. Sellers who wait for "clarity" list into a market where comparable homes have accumulated, buyer urgency has distributed across more options, and list-price ratios have declined incrementally. The Noise Penalty shows up in days on market, list-price ratios, and offer quality.

5. Are buyers still actively looking for homes in Reno-Sparks despite economic uncertainty?

Yes — and this point requires understanding who those buyers are. The primary demand driving Reno-Sparks upper-mid inventory is California equity relocators, data center and technology professionals, and life-transition sellers from higher-cost western states. These buyers are executing decisions with long planning horizons anchored in equity, employment, and life-stage transitions — not in stock market sentiment. They are categorically less affected by the type of economic uncertainty generating national headlines than first-time buyers or buyers whose down payments depend on investment accounts. March 2026 closings in Reno were up 23.2% from February. In Sparks they were up 43.0%. Buyers are not waiting for certainty. They're acting.

6. How do tariffs affect home sellers — not buyers — in Reno-Sparks?

For existing home sellers, tariffs are a structural tailwind, not a headwind. As we covered in detail earlier this year, tariff-related cost increases of approximately $10,900 or more per new home (NAHB estimate) have made new construction a more expensive alternative for buyers who might otherwise have considered it. Every dollar of additional cost a builder must pass through in a new-construction transaction strengthens the competitive position of a well-maintained existing home at similar or lower price. In a market where builders are already redirecting capacity toward data center construction (per EDAWN's 2026 data), the new-construction competition for existing sellers is diminishing on two fronts simultaneously.

7. What are mortgage rates in 2026, and what do they mean for home sales in Reno?

As of April 9, 2026, the 30-year fixed-rate mortgage averaged 6.37% per Freddie Mac's Primary Mortgage Market Survey — down from 6.46% the prior week and 6.62% a year ago. On a $632,000 purchase (Reno's March median) with 20% down, that rate translates to a monthly principal and interest payment of approximately $3,125. MBA forecasts suggest rates near 6.30% through 2026; Fannie Mae projects rates approaching 6.0% by year-end. Lower rates expand the qualifying pool for Reno-Sparks buyers. Combined with the structural supply constraint (1.7 months of inventory), rate improvement tends to produce increased competition for available listings rather than a change in market direction.

8. Is right now actually a good time to sell a home in Reno or Sparks?

Based on the available data, yes — with important qualifications. The data pointing toward a favorable seller environment is specific and verifiable: 1.7 months of supply in Reno, 1.1 in Sparks, 15-day median days to contract, 98.9-99.3% list-price ratios, and a buyer pool anchored in structural economic demand rather than cyclical sentiment. The qualification is that "good time" depends on preparation, pricing accuracy, and execution — a well-prepared home at a realistic price in a low-supply market generates strong outcomes; an overpriced or underprepared listing in the same market does not. The market conditions favor decisive, well-executed listings. They don't compensate for strategic errors.

Check out this article next