This post is for informational purposes only and does not constitute financial, legal, or investment advice. National economic data referenced below is sourced from the Bureau of Labor Statistics (BLS), Freddie Mac Primary Mortgage Market Survey (PMMS), the National Association of Realtors (NAR), Cotality, and the Mortgage Bankers Association (MBA). Local market statistics are sourced from NNRMLS via Domus Analytics, updated March 1, 2026. Mortgage payment figures are illustrative only and exclude taxes, insurance, HOA fees, and other costs. Economic conditions change — consult a licensed real estate professional before making any real estate decision. Kevin Kinney and Robin Renwick are licensed Nevada real estate professionals.

Key Takeaways

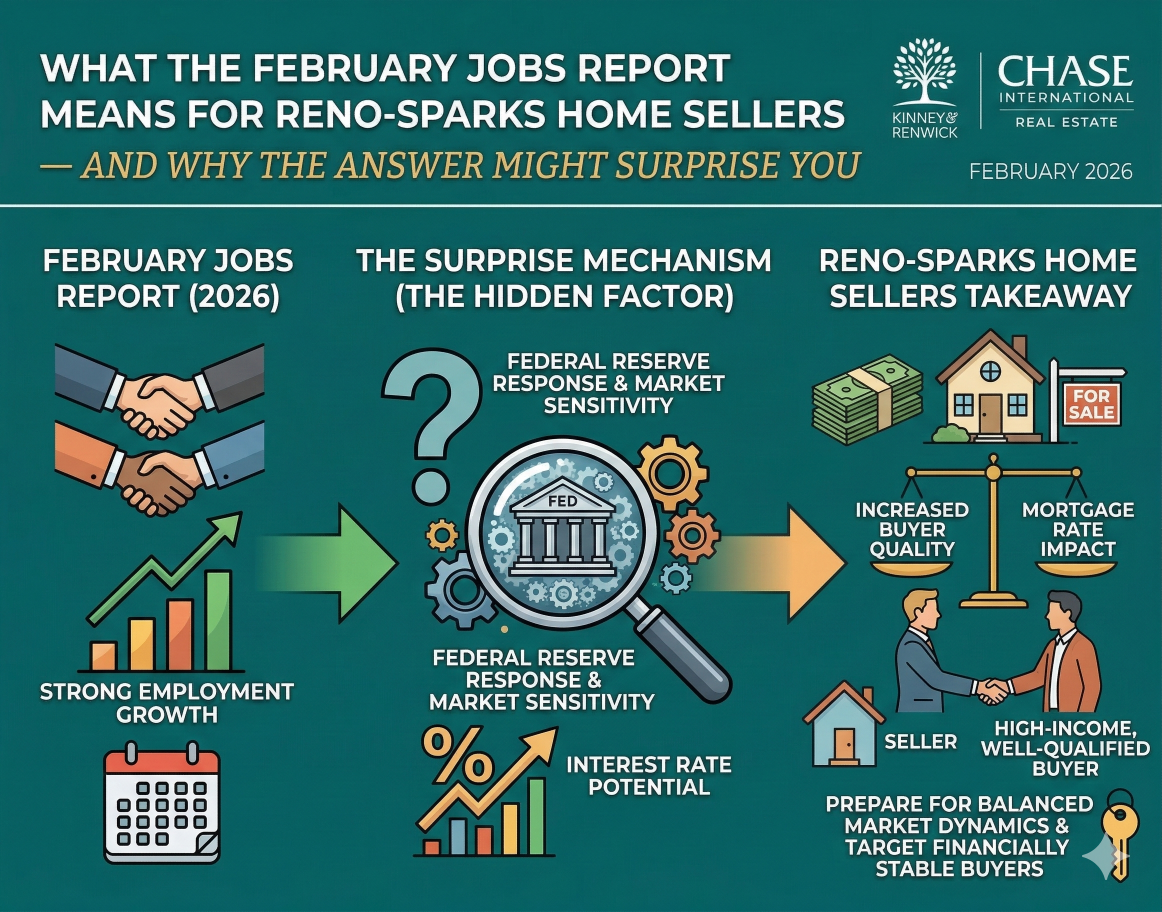

- The February 2026 jobs report — a loss of 92,000 positions nationally — triggered recession fears this week, but the sectors driving that job loss are not the sectors driving Reno-Sparks housing demand.

- Counterintuitively, a weaker national economy may push mortgage rates lower, expanding the buyer pool at the exact moment Reno-Sparks inventory remains historically compressed.

- Reno's median sale price hit $639,000 in February, Sparks held at $534,990, and both cities remain deep in seller's market territory with less than two months of supply — conditions that don't reverse overnight because of a national headline.

- The Reno metro ranked #1 for economic growth out of 949 national metros in EDAWN's 2026 State of the Economy report — structural demand that insulates this market from purely cyclical national trends.

- Sellers who pause to "wait for national clarity" typically list in May or June against significantly more competition, often surrendering the highest-leverage window of the spring market.

If you checked your phone this morning, you saw something that could reasonably make any homeowner put their selling plans on hold.

The Bureau of Labor Statistics reported Friday that the U.S. economy shed 92,000 jobs in February — a catastrophic miss against economist expectations of a 59,000 gain. The unemployment rate ticked up to 4.4%. December's report, previously showing a modest 48,000-job gain, was revised to a loss of 17,000. The economy has now shed jobs in three of the last five months. The Dow dropped more than 600 points this morning. Oil prices have surged to $90 per barrel following the U.S.-Israeli campaign against Iran, raising fresh inflation fears and complicating the Federal Reserve's ability to cut rates. Recession is no longer a fringe forecast — it's the lead story on every financial news outlet this week.

If your instinct is to freeze — to call your plans and wait until the national picture clarifies — that is a completely understandable response. It's also, for a seller in Reno-Sparks right now, probably the wrong one.

That's not a marketing line. It's a data argument. And it runs in three directions at once: what the jobs report actually says about the people buying homes here, what a weakening national economy typically does to mortgage rates, and what the local inventory and pricing data says is happening on the ground in this market regardless of what Wall Street is doing this week.

Let's work through each one.

The Jobs That Were Lost Aren't the Jobs That Buy Homes in Reno-Sparks

The February payroll report shows job losses concentrated in three sectors: healthcare (-28,000, driven primarily by a Kaiser Permanente strike that sidelined more than 30,000 workers in Hawaii and California during the BLS survey week — a strike that has since been resolved), leisure and hospitality (-27,000), and construction and manufacturing (-23,000). The only sectors that added jobs in February were financial activities, wholesale trade, retail trade, utilities, and other services.

This matters because it tells you something specific about who drove that headline number — and whether that population overlaps with the buyer pool currently competing for quality homes in Somersett, Damonte Ranch, Caughlin Ranch, and South Meadows.

The answer is: not substantially. The Kaiser strike is a one-month statistical distortion; Kaiser itself has acknowledged the dispute is resolved and those workers have returned. Leisure and hospitality losses reflect service-sector softness — these are not the households arriving from the Bay Area or Sacramento with $400,000 to $600,000 in equity from a recently sold California home, looking to eliminate state income tax and purchase at a fraction of their prior market's prices. Construction and manufacturing losses are real, but they reflect national capacity constraints and tariff headwinds — again, not the demographic driving inbound relocation to the Reno metropolitan area.

The buyer most likely to walk through a quality listing in Northwest Reno or ArrowCreek this spring is employed in technology, data infrastructure, business services, finance, or some professional field that transferred remotely or followed one of the 15 companies EDAWN tracked as announcing relocations or expansions in the Reno metro in 2025. That profile didn't get a pink slip in February. Those jobs weren't in the payroll loss column.

Sam Williamson, senior economist at First American, described jobs growth in February as having "fizzled," noting "little evidence of renewed momentum in the labor market." That's accurate nationally. What it doesn't describe is the specific economic engine operating underneath the Reno-Sparks housing market — an engine that EDAWN documented in February as having generated $534 million in new business investment, 593 jobs at an average salary of $76,800, and the nation's first-ranked metropolitan area for economic growth out of 949 metros tracked.

These are not the same economy.

A Counterintuitive Turn: Weak Jobs Data and What It Does to Mortgage Rates

Here's where the analysis gets interesting for sellers who are willing to think beyond the headline.

When the national economy weakens, the Federal Reserve typically cuts interest rates to stimulate growth. Rate cuts flow through to bond markets, which move mortgage rates. The same economic deterioration that is causing recession anxiety this week is also, in the view of several respected economists, making the path toward lower mortgage rates more likely — not less.

Chen Zhao, Head of Economics Research at Redfin, put it directly in the days following the jobs report: a weaker labor market will lead the Fed to cut interest rates twice this year, and the current environment supports brief dips into the 5% range for mortgage rates. Daryl Fairweather, Redfin's Chief Economist, has been consistent in her view that Fed cuts will keep rates in the low-6% range for 2026, with meaningful downward pressure if economic softness continues.

Freddie Mac's Chief Economist Sam Khater noted on March 5th, as the 30-year fixed rate averaged 6.00%, that rates are now down nearly a full percentage point from this time in 2024 — and that purchase applications are already running ahead of last year's pace as a result.

What does a percentage point drop in mortgage rates actually mean for buyer demand? NAR research quantifies it directly: nationally, a one-percentage-point reduction in the 30-year rate expands the pool of households that can qualify to buy by approximately 5.5 million — including roughly 1.6 million renters who become first-time buyer candidates. Not all of those households buy immediately, but the demand expansion is real, it's fast-moving, and it flows directly into markets like Reno-Sparks where qualified relocation buyers are already active.

Put it together: the same weak jobs report that is triggering seller hesitation today is the data point most likely to push mortgage rates lower over the next 60 to 90 days. Lower rates mean more qualified buyers. More qualified buyers mean more competition for the 2.1 months of supply in Reno and the 1.6 months of supply in Sparks. That's not a scenario where sellers benefit from waiting.

There is a complicating factor, and it deserves honest acknowledgment. The Iran conflict has pushed oil prices toward $90 per barrel, and elevated energy prices are inflationary. Joel Kan, MBA's Deputy Chief Economist, stated directly that given the heightened inflation risk, the Fed is unlikely to cut rates immediately, and that MBA is forecasting mortgage rates to remain in the 6% to 6.5% range for the foreseeable future. The stagflation scenario — weaker jobs combined with rising prices — creates real uncertainty for the Fed's timeline.

What that means for sellers isn't that the market will weaken. It means rates may move slowly rather than dramatically. In Reno-Sparks, where the rate at 6.00% is already spurring purchase applications above last year's pace and where supply remains historically constrained, the market doesn't need a dramatic rate drop to stay seller-favorable. It's already seller-favorable. We published the February numbers two weeks ago — $639,000 median in Reno, a list-price ratio of 98.6%, 17 days to contract in Sparks — and those numbers were generated in a rate environment nearly identical to today's.

What the National "Two-Speed Market" Story Is Actually Saying About Reno

Cotality Chief Economist Dr. Selma Hepp has been describing a "two-speed housing market" in 2026: coastal and Sunbelt regions experiencing price corrections while Midwest and Northeast markets remain resilient. Cotality's most recent data shows that 22 of the top 100 U.S. metros are now experiencing year-over-year price declines — led by Florida markets like Cape Coral (-10.2%), North Port-Sarasota (-8.9%), and Western metros including Colorado (-1.31%), Utah (-1.11%), Arizona (-0.61%), and California (-0.15%). National price appreciation has slowed to 0.7% year-over-year as of January — the lowest reading since the post-Great Recession recovery began.

For a seller reading national headlines, this sounds alarming. If you don't live inside the local data, it's easy to assume Reno is in that list somewhere. It isn't.

Reno's February median sale price of $639,000 represents 3.9% appreciation above February 2025. Sparks at $534,990 held 1.9% above year-ago levels. Both cities are seeing seller-favorable days-on-market, full-price offers, and sub-two-month supply. The markets that are correcting — Florida, Arizona, parts of California — overbuilt aggressively during the pandemic era and are now absorbing that excess inventory. Reno-Sparks did not overbuild. The supply gap here is structural, not cyclical, and it doesn't close because a jobs report came in weak in February.

The deeper point is worth sitting with. The national narrative of a "two-speed market" is actually good news for sellers in this specific market — because it confirms that price corrections are geographically concentrated in places with very different supply and demand dynamics. Reno-Sparks has 2.1 months of supply. Cape Coral has enough inventory to drown in. These are not the same market, and national headlines that blend them together are doing sellers here a disservice.

What the EDAWN Data Says About Structural Demand

At EDAWN's 2026 State of the Economy presentation on February 5th — which Kevin attended in person — the picture drawn for the Reno Metropolitan Statistical Area had almost nothing to do with the sectors shedding jobs nationally in February.

The Reno metro ranked number one for economic growth out of 949 national metros. Reno and Las Vegas have been identified as the number one fastest-growing data center hub in the United States, with growth of up to 953% — ahead of Salt Lake City, Phoenix, Atlanta, Dallas-Fort Worth, Chicago, Austin, and Denver. Data center construction spending is expected to rise 23% in 2026. The Reno metro logged $534 million in new business investment last year, attracted 15 companies announcing relocations or expansions, and produced the area's first tech unicorn. Venture capital secured totaled $1 billion over the past year. EDAWN's site visit volume — 176 visits, roughly 14 per month — ranks in the top 1% nationally.

This is the demand backdrop for a quality home in Wingfield Springs, Double Diamond, or Old Southwest Reno. The household relocating to purchase that home isn't watching the national jobs report and reconsidering their move because healthcare workers went on strike in California. They're watching it the same way any informed adult watches economic news — with awareness, not panic — and then going back to their timeline, which is driven by life decisions, not market headlines.

NAR's demographic data on sellers is instructive here as well. The median seller is 64 years old and has owned their home for 11 years. Eighty-one percent have no children under 18 at home. These are empty nesters moving through a life transition — toward a smaller footprint, a different city, a simpler lifestyle, or proximity to family. These transitions are not postponed because the February jobs report was weak. They are postponed when sellers convince themselves that "waiting" is a financial strategy — when in most cases, it isn't.

The Real Cost of Waiting That Sellers Underestimate

There's a specific version of "waiting for clarity" that plays out in Reno-Sparks every spring, and it has a consistent outcome.

A seller in Caughlin Ranch decides in early March that the national news is too uncertain. They push their timeline to May. By May, mortgage applications have risen further as spring demand accelerates. But so has competition — other sellers who made the same calculation, or who simply delayed for other reasons, are now listing at the same moment. The window of maximum leverage — when buyer demand is rising and competing supply is still compressed — has narrowed. The home that would have received two or three serious offers in March may now receive one. Not because the market collapsed, but because the competitive environment for buyers shifted.

We wrote about this dynamic in detail when we covered spring timing earlier this month — the data from February shows a market that doesn't wait for sellers to feel ready. Sparks contracts are happening in 17 days. Reno buyers are paying 98.6% of list price. That's the current baseline, today, with a weak national jobs report on the front page of every financial publication.

The question isn't whether the national economy is softening. It clearly is. The question is whether that softening is doing anything material to the supply of quality homes in South Meadows, Spanish Springs, or the Northwest Reno corridor, or to the pool of qualified buyers who are actively competing for those homes. Based on the February NNRMLS data, the answer to both is no.

What the national uncertainty does, consistently and predictably, is cause sellers who own quality homes in strong markets to hesitate. And in a market with 2.1 months of supply, the seller who hesitates is giving the seller who doesn't a meaningful competitive advantage — not just in getting an offer, but in getting the right offer from the right buyer at the right price.

The Strategic Frame for Sellers Right Now

Think about this from the buyer's perspective for a moment — specifically, the buyer most likely to purchase a quality Reno-Sparks home in the $550,000 to $800,000 range this spring.

That buyer has spent the last several months preparing. They've sold or are under contract on a California, Oregon, or Washington home. They've watched mortgage rates at 6.00% and made their financial calculations. They've read about Reno's economic growth, done neighborhood research in Somersett and Damonte Ranch, and either visited or are planning to visit within the next few weeks. They understand the equity math — what their Bay Area or Sacramento home sale means for purchasing power in Northern Nevada. We broke that math down in depth when we covered who's actually buying Reno-Sparks homes in 2026.

That buyer does not pause their relocation because of a February jobs report. They may pause if rates spike dramatically or if the local market shifts in ways visible in the data. But the data doesn't show that. The data shows a compressed, seller-favorable market with rising prices, quick contracts, and well-qualified buyers executing at or near full list price.

For sellers who own quality homes — especially those in the life-transition category that represents the majority of current seller activity — the strategic reading of this moment is the opposite of hesitation. The national uncertainty is suppressing seller entry, which means the competition you might have faced from other listings is also waiting. That creates a window.

The sellers who consistently do best in this market are not the ones who time it perfectly based on national headlines. They're the ones who enter prepared, priced correctly, and presented professionally — and who do so while the competition is still deciding whether to wait.

If you're considering a sale and want to think through what these conditions mean for your specific situation, we're happy to have a thoughtful conversation about your goals. Kevin Kinney | 775-391-8402 · Robin Renwick | 775-813-1255

FAQs

1. Should Reno-Sparks homeowners be worried about the February jobs report and a potential recession? National economic softening warrants attention, but the sectors driving February's job losses — healthcare (primarily a Kaiser Permanente strike that has since been resolved), leisure and hospitality, and manufacturing — are not the sectors that drive Reno-Sparks housing demand. The Reno metro ranked #1 for economic growth out of 949 national metros in EDAWN's 2026 report, supported by data center expansion, technology relocation, and venture capital investment that run on different economic tracks than the national payroll figures.

2. Could the weak jobs report actually lower mortgage rates and help Reno sellers? Counterintuitively, yes — that's a credible scenario. A weaker labor market signals to the Federal Reserve that rate cuts may be needed to prevent a deeper slowdown. Chen Zhao, Head of Economics Research at Redfin, noted directly that a weaker labor market is expected to lead the Fed to cut rates twice in 2026. Lower rates expand the qualified buyer pool — NAR data shows that each percentage point drop in the 30-year mortgage rate adds roughly 5.5 million households to the buyer market nationally. There's an important caveat: rising oil prices from the Iran conflict introduce inflation risk that complicates the Fed's timing. Rates may stay elevated longer than some forecasts suggest. But the directional pressure, if the economy softens further, is toward lower rates — which benefits Reno sellers.

3. Is Reno-Sparks part of the national "two-speed market" correction? No. The markets experiencing year-over-year price declines in 2026 — Florida, Colorado, Utah, Arizona, California — share a common feature: significant inventory increases following pandemic-era overbuilding. Reno-Sparks has the opposite condition. Supply in Reno sits at 2.1 months; Sparks at 1.6 months. Both are deep in seller's market territory. Reno's February median price of $639,000 is 3.9% above February 2025. These are not correction conditions.

4. How are Reno-Sparks home prices holding up in early 2026 despite national softness? February 2026 data from NNRMLS via Domus Analytics shows Reno's median single-family sale price at $639,000 — up 11.1% from January and 3.9% above February 2025. Sparks held at $534,990, up 1.9% from January and 1.9% year-over-year. Sellers received 98.6% to 99.1% of list price in both markets. These numbers were generated in the same rate environment that exists today.

5. Is the spring 2026 market in Reno-Sparks still favorable for sellers? The February data doesn't describe a market building toward spring — it describes a market already executing spring-level metrics in mid-winter. Sparks contracts are closing in 17 days. Supply is at or near historic lows. Buyer affordability, by NAR's Housing Affordability Index, is at its best level since March 2022. The window is open. The question is whether sellers choose to use it or defer to competition that will enter later.

6. What types of buyers are still active in the Reno-Sparks market right now? The core demand driver is well-capitalized relocation from California, Oregon, and Washington — buyers converting significant equity from higher-priced markets into Reno-Sparks purchasing power. These buyers are motivated by structural factors: no Nevada state income tax, lower property taxes, Reno's #1-ranked economic growth, and quality of life. They are not the demographic represented in national labor market softness data. We detailed this buyer profile and the equity math behind it in our breakdown of who's buying Reno-Sparks homes in 2026.

7. If I wait until May or June to list, what changes? Two things typically happen when sellers wait for spring "certainty." First, more competing listings enter the market simultaneously, which gives buyers more options and reduces the negotiating leverage that sellers currently hold. Second, the first weeks on market — historically when the highest-motivated buyers are most active — occur in a more crowded field. A home that might have drawn multiple offers in March may draw one in May, not because the market deteriorated, but because the competitive environment for buyers shifted. Sellers who enter the market earlier, while competing supply is still compressed, consistently capture better outcomes.

8. What is the EDAWN data and why does it matter for home sellers in Reno-Sparks? EDAWN (Economic Development Authority of Western Nevada) produces an annual State of the Economy presentation combining regional business investment data, job creation figures, migration patterns, and corporate relocation activity. The 2026 report, presented February 5th, documented that the Reno metro ranked #1 for economic growth among 949 U.S. metros, attracted $534 million in new business investment, logged the region's first tech unicorn, and reached $1 billion in venture capital investment over the prior year. This is the economic engine underneath Reno-Sparks housing demand — and it is structurally separate from the national payroll trends that drove the February jobs report headline.

Check out this article next