Disclaimer: This post is for informational purposes only and does not constitute financial, legal, or investment advice. Market data is sourced from the NNRMLS via Domus Analytics, updated March 1, 2026. Conditions change — consult a licensed real estate professional before making any real estate decision. Kevin Kinney and Robin Renwick are licensed Nevada real estate professionals.

Key Takeaways

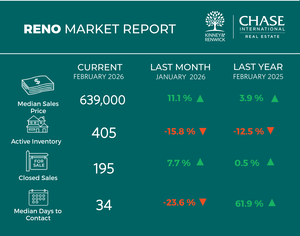

Reno's median sales price reached $639,000 in February — up 11.1% from January and 3.9% year over year

- Sparks homes went under contract in a median of 17 days — down 48.5% from January alone

- Active inventory in Sparks is down 36.4% year over year — 164 homes for an entire city

- Months supply: 2.1 in Reno, 1.6 in Sparks — both deep in seller's market territory

- Sellers received 98.6–99.1% of list price — full-price offers are the expectation, not the exception

- Combined active inventory across Reno and Sparks: approximately 569 homes for the entire metro

- The Reno metro holds the #1 economic growth ranking out of 949 national metros (EDAWN, February 2026)

You've been told to wait for spring. List in March, hold out for April, let the buyers come out before you make your move. It's the conventional wisdom passed around at dinner parties and shared in group texts, and most years it has at least some basis in reality.

February 2026 in Reno-Sparks didn't get the memo.

The Northern Nevada Regional MLS data, updated March 1, tells a story that should have every serious seller paying attention right now. Inventory is tightening at a pace that has no seasonal explanation. Prices are accelerating. Homes are going under contract faster than they did in January, and in some cases faster than they did a year ago. Spring didn't arrive in March this year. It arrived in February, quietly and without announcement, and the data confirms it.

What's Happening in Reno

Reno's median sales price in February came in at $639,000 — an 11.1% jump from January and 3.9% above where prices stood in February 2025. That kind of month-over-month acceleration in the dead of winter isn't typical seasonal behavior. It reflects genuine compression: fewer homes available, more buyers competing for them, and a willingness to pay at or near asking price to secure a contract.

Active inventory in Reno stood at 405 homes — down 15.8% from January and 12.5% below February 2025 levels. New listings fell 9.3% from the prior month and 7.9% year over year, meaning the pipeline isn't refilling fast enough to keep pace with demand. The result is a months supply of inventory at 2.1, down 21.8% from January and 13.0% below where it was a year ago. For reference, economists and housing analysts define a balanced market as four to six months of supply. Reno is operating at less than half of that lower bound. Sellers hold the leverage here, and the numbers reflect it.

Buyers in Reno are paying $333 per square foot at the median — up 2.5% from January — and closing at 98.6% of list price. That last figure has held flat from January and is actually up 0.2% from a year ago, which tells you something meaningful about how buyers are approaching offers. In a market where homes are listed, positioned, and priced correctly, they're not negotiating down. They're meeting the number.

The median days to contract came in at 34, which is faster than January's pace by 23.6% and worth putting in full context. A year ago in February 2025, Reno's median days to contract was closer to 21 days — and that 61.9% year-over-year increase is the one figure in this report that deserves honest discussion rather than a spin. Today's market is active and demand is real, but it isn't the compressed frenzy of early 2025. What that means practically: the listings that went under contract in under two weeks last month were almost certainly well-prepared and priced correctly. The ones that sat longer were not. In a 34-day median environment, preparation and positioning aren't nice-to-haves. They're the determining factor between a clean, competitive sale and a price reduction conversation three weeks in.

For sellers in Somersett, Northwest Reno, and Caughlin Ranch, this is the environment where the investment in presentation pays its highest return. We've covered the ROI of staging in this market in detail — and the case for it only strengthens when buyers have limited options and are comparing every home they see against the handful of well-presented alternatives currently available.

What's Happening in Sparks

If Reno's numbers are strong, Sparks is operating on another level entirely.

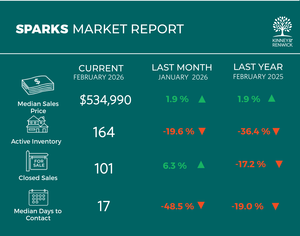

The median sales price in Sparks reached $534,990 in February — up 1.9% from January and 1.9% year over year. Steady appreciation, not a dramatic spike. But the metrics beneath that price figure reveal a market under significant pressure.

Start with inventory. Active listings in Sparks: 164 homes. That's down 19.6% from January and down 36.4% from February 2025. For a city of Sparks' size, 164 active single-family listings represents an extremely constrained supply picture. New listings fell 23.8% from January and 31.7% year over year — meaning sellers aren't entering the market in any volume, and what little inventory exists is being absorbed quickly.

The months supply figure is 1.6, down 24.4% from January and 23.2% below a year ago. Housing economists classify anything below 2.0 months as acute scarcity that typically produces competitive conditions and sustained upward price pressure. Sparks isn't approaching that threshold — it's well past it, and has been for consecutive months.

The speed of the market confirms it. Sparks homes went under contract in a median of 17 days in February — down 48.5% from January and 19.0% faster than February 2025. At 17 days, the median home in Sparks is going under contract in under three weeks. Sellers received 99.1% of list price at $307 per square foot, with both metrics improving from January and year-over-year.

For homeowners in Wingfield Springs, South Meadows, and Spanish Springs who have been considering their timing, these numbers carry a straightforward implication. With 164 active listings serving an entire city and homes accepting contracts in 17 days, a well-prepared listing in this market isn't waiting for offers. It's selecting from them.

The Bigger Economic Picture

Housing statistics don't exist in a vacuum. The inventory compression and price appreciation in Reno-Sparks right now aren't random — they're downstream of economic conditions that have been building for years and show no sign of reversing.

Earlier this year, the Economic Development Authority of Western Nevada presented its annual State of the Economy report to regional business leaders. The findings contextualize everything happening in this housing market. The Reno metro ranked #1 out of 949 national metros for economic growth. Inbound migration places Reno in the top ten nationally. Data center construction in the region has expanded by roughly 953% in recent years, with major operations from technology companies anchoring a commercial base that's driving both employment growth and population relocation at scale.

This isn't a speculative housing story. It's a story about a city whose economic foundation is attracting people with the income and equity to purchase quality homes at significant price points. The buyer arriving in Reno from the Bay Area or Seattle with $500,000 or $600,000 in accumulated equity and a household income that makes Nevada's zero state income tax feel like an annual raise isn't a marginal buyer. They're a motivated, financially capable buyer choosing Reno because the numbers make sense. We explored that buyer pool in depth in our analysis of California equity and what it means for local sellers — and February's data reinforces every element of that picture.

Combine that demand profile with a combined metro inventory of approximately 569 homes across Reno and Sparks, and the structural tension underneath these statistics becomes clear. There is not enough supply to meet qualified demand at current levels. New construction won't close that gap this spring — developable land in the Reno-Sparks metro is constrained by federal land ownership patterns, permitting timelines, and cost pressures that have only intensified. We covered the specific dynamic of how tariffs are currently working in favor of existing home sellers in a recent post — the short version is that new construction is getting more expensive while existing homes remain competitively priced. That gap is a structural advantage for sellers of quality existing homes in this market.

What This Means If You're Thinking About Selling

The question we hear most often from sellers in late winter is some version of: should I wait? Is it worth holding off until the market peaks?

Here's what the February data actually says. The market is already operating at peak leverage for sellers in most price segments. Inventory is compressing, not expanding. Prices are rising month over month. Contracts are accelerating. The first two to three weeks after a listing goes live remain the highest-leverage window in any sale — when buyer attention is most concentrated, when offers are most competitive, and when sellers retain the strongest negotiating position. That window doesn't improve meaningfully by waiting until May or June. In most cases, a well-prepared listing entering the market in March or April captures peak spring demand before competing listings increase supply.

What separates a listing that closes strong from one that doesn't in this environment comes down to preparation and pricing. The homes going under contract in under two weeks are earning that result — they're priced with precision, presented at their best, and positioned with a strategy that accounts for who the buyer is and what they're comparing. The homes sitting beyond the median are not. We've covered the specific mistakes that cost Reno-Sparks sellers money in detail in our spring seller guide — and the February data validates each one.

For sellers who have been waiting for certainty, here it is: 2.1 months of supply in Reno, 1.6 in Sparks, prices up, contracts accelerating, and qualified buyers actively looking. The window is open.

What This Means If You're Thinking About Buying

The honest message for buyers in this market is that preparation isn't optional. With Sparks homes going under contract in 17 days and Reno at 34, there is no time to sort out financing mid-search. Pre-approval needs to be complete before the first showing. For buyers using significant equity from an out-of-state sale toward a Reno-Sparks purchase, having that capital picture clearly defined before entering the market is what gives you the ability to move decisively when the right home appears.

Mortgage rates have remained cooperative. Freddie Mac's recent data has 30-year fixed rates holding near their lowest levels in approximately three years — and the rate environment we've been tracking since late 2025 continues to support qualified buyers who are in a position to act.

For anyone evaluating a relocation from California, Washington, or Oregon and trying to understand what the financial picture actually looks like — equity conversion, purchasing power by neighborhood, tax environment — our 2026 relocation guide walks through the math in real, transaction-level terms.

Looking Ahead

March data won't be available until early April, but the trajectory entering spring is clear. Inventory is tightening. Demand is active. The economic conditions drawing qualified buyers to this metro aren't seasonal — they're structural, and they're not reversing. The 2026 spring market in Reno-Sparks is not building toward something. It's already here.

If you own a quality home in this market and have been trying to time your entry, February gave you the answer. If you're a buyer trying to find your footing before the busiest months arrive, the time to get positioned is now.

For sellers and buyers who want a thoughtful conversation about what these numbers mean for their specific situation, we're glad to have it.

Kevin Kinney | Robin Renwick Kinney & Renwick Team | Chase International Real Estate 📞 775.258.2949 | 📧 [email protected] kinneyandrenwickteam.com

FAQs

What is the current median home price in Reno in 2026? As of February 2026, the median sales price for single-family homes in Reno is $639,000, up 11.1% from January 2026 and 3.9% above February 2025, according to NNRMLS data updated March 1, 2026.

What is the current median home price in Sparks in 2026? The median sales price in Sparks reached $534,990 in February 2026 — up 1.9% from January 2026 and 1.9% year over year, per NNRMLS data updated March 1, 2026.

How long are homes sitting on the market in Reno-Sparks right now? In February 2026, the median days to contract was 34 days in Reno and 17 days in Sparks. Sparks homes are moving nearly twice as fast as a year ago, while Reno's pace is quicker than January but slower than February 2025's compressed pace of approximately 21 days.

Is it a buyer's or seller's market in Reno-Sparks in 2026? It's firmly a seller's market in both cities. Reno has 2.1 months of supply and Sparks has 1.6 months — both well below the 4-to-6-month range that defines a balanced market. Sellers are receiving 98.6% to 99.1% of list price.

Is home inventory increasing or decreasing in Reno-Sparks? Inventory is decreasing in both cities. Active listings in Reno fell 15.8% from January and 12.5% year over year. In Sparks, active inventory dropped 19.6% from January and a significant 36.4% from February 2025. Combined metro inventory sits at approximately 569 homes.

Is spring 2026 a good time to sell a home in Reno or Sparks? The February data strongly suggests yes. Inventory is compressed, prices are rising, contracts are accelerating, and qualified buyer demand is active. The first weeks on market remain the highest-leverage window — sellers who enter the spring market prepared and priced correctly are seeing full-price and near-full-price offers.

What economic factors are driving the Reno-Sparks housing market? The Reno metro ranked #1 out of 949 national metros for economic growth according to the EDAWN February 2026 State of the Economy report. Top-ten inbound migration nationally, sustained data center and tech sector expansion, and significant California equity relocation are the primary demand drivers.

What should buyers know about the Reno-Sparks market in February 2026? Buyers need to be fully pre-approved before searching. With Sparks at 17-day median contracts and Reno at 34 days, there's no time to arrange financing after finding a home. Buyers using California or Pacific Northwest equity have strong purchasing power in this market, but preparation and decisiveness are essential.

Check out this article next